Tax Benefits for Employers: Navigating 401k and Pension Contributions

Employers always seek ways to optimize tax benefits while supporting employee retirement. To do so, they must understand the complexities of 401k and pension contributions.

As an employer, you have several options for maximizing tax advantages and employee benefits. This article simplifies the process and offers clear guidance on optimizing 401k and pension contributions.

Inside, you'll find:

The tax benefits of offering 401k and pension plans to employees.

Strategies for structuring contributions to maximize tax advantages.

Common pitfalls to avoid when managing retirement plans.

Expert tips for staying compliant with IRS regulations.

Ready to unlock the full potential of employer tax benefits? Let's dive into the details of 401k and pension contributions together. Keep reading to gain valuable insights and ensure your financial strategy is optimized.

Understanding 401k Contributions and Tax Benefits

Working through 401k tax benefits for employers involves precision. And each decision affects your business's financial health. Here's how to manage and optimize your 401k contributions effectively.

Immediate Tax Deductions

Contributions to 401k plans are tax-deductible. The money you contribute on behalf of your employees directly reduces your taxable income.

The process is straightforward. Your taxable income decreases by an equivalent amount for every dollar you contribute.

Pro tip: So act wisely. Maximize these contributions to fully leverage the tax benefits.

Tax Credits for New Plans

There are additional incentives for starting a new 401k plan. The SECURE Act introduced tax credits, which can total up to $5,000 per year for the first three years.

The purpose is clear: to offset the costs of establishing a new retirement plan. Small businesses benefit most as It eases the initial financial burden.

Contribution Limits

Be aware of the annual contribution limits because they adjust for inflation.

In 2024, you can contribute up to $69,000 per employee, including your contributions and any employee deferrals.

Pro tip: Monitoring these limits is crucial. They influence how much tax benefit you can realize each year.

Catch-Up Contributions

Employees over 50 can make catch-up contributions in addition to the standard limit. The current catch-up limit is $7,500.

Pro tip: This provides an opportunity. Encourage older employees to take advantage of this as it increases their retirement savings and offers higher deductible contributions.

Loan Provisions

401k plans can include loan provisions. These allow employees to borrow from their savings. It's a benefit and can make your plan more attractive. However, manage this carefully. Loan defaults can have tax implications for the employee.

Vesting Schedules

Implement vesting schedules. In a nutshell, these control when employees own your contributions.

But here’s the thing: clarity in vesting schedules is essential. They impact employee retention and influence their long-term investment in your company.

Compliance

The IRS imposes strict rules on 401k contributions and administration. Besides, non-compliance results in penalties.

Pro tip: Regular reviews and audits of your plan are mandatory to ensure compliance. More importantly, they maintain the integrity of your plan.

Insider Tip:

We advocate a proactive approach to managing 401k plans. We've found that syncing contribution strategies with business cash flow cycles maximizes benefits. Our clients who align their 401k contributions with their revenue peaks and troughs optimize their cash flow. Even better, they maximize their tax advantages. This approach demands close monitoring of financial cycles. But it pays off. Consider this strategy to enhance your financial planning and tax benefits.

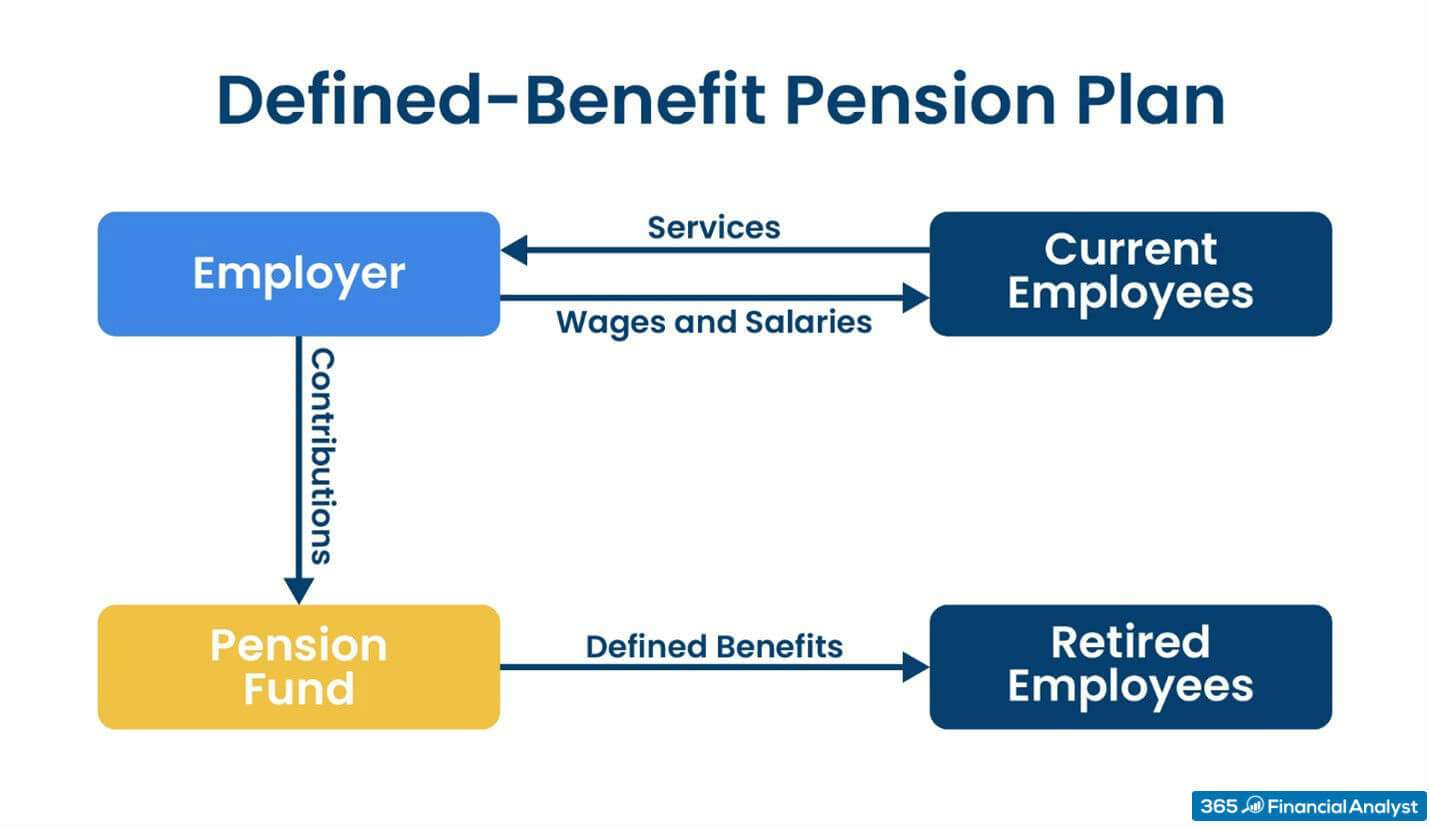

Understanding Pension Plan Contributions and Tax Benefits

Navigating pension plan tax benefits requires understanding and strategy. Here’s how to optimize your pension contributions:

Immediate Tax Deductions

Contributions to pension plans offer immediate tax relief. Basically, each dollar contributed reduces your taxable income for the year.

This direct benefit is reflected in lower corporate taxes. Take advantage of this and maximize contributions to enhance these deductions.

Tax-Deferred Growth

The investments within pension plans grow tax-deferred. In other words, no taxes apply on the earnings until distributions begin.

This benefits you because the fund can grow without the immediate burden of taxes. Over time, this compound growth will significantly increase the retirement fund.

Non-Discrimination Tests

Pension plans must comply with non-discrimination tests. These ensure benefits do not favor highly compensated employees disproportionately.

Remember: Understanding these rules is essential. So, structure your contributions correctly. And remember, compliance is mandatory to maintain tax-advantaged status.

Funding Requirements

Defined benefit plans require regular contributions. These ensure the plan can meet its future obligations. The IRS mandates these contributions, and failing to meet funding requirements results in penalties.

Remember: Stay informed. Ensure your contributions are timely and sufficient.

Plan Limits

Know the annual benefit limits. For 2024, the yearly maximum benefit allowed under a defined benefit plan is $265,000.

Remember: This limit is crucial. It caps the benefit amount you can promise any employee upon retirement.

Vesting Schedules

Implement clear vesting schedules. These schedules define when employees claim ownership of contributions.

But they also have an awesome advantage for your company:

Vesting schedules can influence employee retention and encourage long-term commitment.

Pro tip: To maximize this benefit, design these schedules to align with your strategic goals.

Actuarial Calculations

Defined benefit plans involve complex actuarial calculations, which determine required contributions based on retirement benefits.

Pro tip: Hire competent actuaries whose expertise ensures your plan meets all financial and regulatory requirements.

Plan Termination Insurance

Pension plans are insured by the Pension Benefit Guaranty Corporation (PBGC), a federal agency that protects plan participants' retirement incomes.

Remember: Understand the premiums. They are mandatory and calculated based on plan factors.

Insider Tip:

We've learned the importance of leveraging advanced funding techniques for pension plans. Take, for example, "credit balancing." This approach involves overfunding the pension plan in years when the business is particularly profitable. These excess contributions can be carried forward to offset required contributions in leaner years.

This strategy ensures that the plan remains well-funded and compliant. It also provides significant tax planning advantages by smoothing out tax-deductible contributions over time, leading to more predictable financial outcomes.

We recommend considering this proactive funding strategy to enhance the financial stability of your pension plan and gain greater control over your annual tax liabilities.

Strategies for Maximizing Tax Benefits

To maximize tax benefits from 401k and pension plans, consider these strategic approaches:

Segment Employee Groups: Customize contributions based on employee segments. Differentiate between high earners and entry-level positions. Tailor your contributions to maximize benefits for both groups and maintain plan compliance. This strategy enhances the appeal of your retirement benefits across the workforce.

Optimize Plan Design: Choose between a traditional 401k, a Roth 401k, or a combination of both. Traditional contributions offer upfront tax deductions, while Roth contributions provide tax-free growth. Analyzing your employees' current tax situations helps decide the best mix, which maximizes tax efficiency for the company and the employees.

Leverage State-Specific Advantages: Some states offer additional benefits for retirement plan contributions. Explore these opportunities. Incorporate state-specific incentives into your retirement plan strategy. This can lead to further reductions in state tax liabilities.

Consider Automatic Enrollment: Implement automatic enrollment in your 401k plan because it increases participation rates. Higher employee participation can lead to larger tax-deferred contributions company-wide. This boosts your business's overall tax savings.

Use Vesting Schedules as Incentives: We mentioned these before, but we’ll do it again here because we think they’re really amazing. So, implement extended vesting schedules. Remember, these schedules can act as a retention tool. Basically, they provide tax benefits over an extended period and bind employees to your company, reducing turnover.

Implement Year-End Bonuses into Plans: Direct year-end bonuses into retirement plans. This move benefits both employees and employers. Here’s why that works. Employees increase their retirement savings, and employers (you) gain from additional tax-deductible contributions.

Regular Benchmarking Against Industry Standards: Conduct regular benchmarking of your plan against industry standards. That’s to ensure it remains competitive and cost-effective. Then, you can make adjustments based on benchmarking to improve your tax benefits and plan performance.

Engage in Proactive Fiscal Policy Monitoring: Stay informed about changes in tax laws and fiscal policies that impact retirement plans. Adjust your strategies accordingly to take advantage of new tax incentives or avoid new penalties.

Insider Tip:

We've discovered that proactive scenario planning can significantly enhance tax benefits for employers managing 401k and pension plans. We conduct annual scenario planning sessions, where we simulate various contribution and investment scenarios under current tax laws.

This practice allows us to anticipate changes in our tax obligations and adjust our retirement plan contributions accordingly. That’s how we maximize tax efficiency.

All employers who adopt this approach can adapt more readily to regulatory changes and economic fluctuations, ensuring optimal financial outcomes for the business and its employees.

So, we recommend you also incorporate this strategic forecasting into your annual financial planning to maintain a robust, tax-efficient retirement plan.

Legal and Compliance Considerations

Understanding legal and compliance considerations for 401k and pension plan contributions demands diligence. Here's what you need to know:

Familiarize with ERISA Requirements: The Employee Retirement Income Security Act (ERISA) sets standards for pension and health plans in private industry. ERISA requires transparency. It mandates detailed reporting and disclosure to government entities and plan participants. And obviously, compliance is not optional.

Adhere to IRS Regulations: The Internal Revenue Service (IRS, in case you forgot the acronym) regulates all tax aspects of 401k and pension plans. So, you must ensure timely and accurate contributions. The IRS also sets contribution limits. Exceed these, and you face penalties.

Understand Department of Labor (DOL) Rules: The DOL enforces rules concerning the economic management of plans. These include how you handle plan funds and fiduciary responsibilities. As a plan sponsor, you must act in the participant's best interests. Breaches can lead to serious repercussions.

Annual Form 5500 Filing: You must file Form 5500 annually. This form reports plan information to the IRS and DOL. Remember, accuracy is critical. Mistakes or omissions can trigger audits, and they complicate compliance.

Conduct Regular Plan Audits: You require an annual financial audit if your plan covers over 100 participants. And you need an independent auditor for this. The audit ensures the plan's operations comply with legal mandates and verifies its financial health.Maintain Fiduciary Compliance: Fiduciary responsibility is a core component of plan management. In other words, you must ensure that all decisions favor the plan participants. This involves prudent investments and reasonable plan expenses. Non-compliance can lead to fines or litigation.

Monitor Contributions and Limits: Track employee contributions and overall plan limits. The IRS and DOL watch these figures closely. Accurate record-keeping is essential as it ensures you meet contribution requirements without exceeding limits.

Handle Claims and Appeals Properly: You must have a clear process for handling claims and appeals. For example, participants must have access to a fair and timely process. This is part of ERISA’s requirements. Failure to comply can lead to disputes or federal action.

Stay Updated on Changes: Tax laws and regulations around retirement plans can change. So, stay informed. Changes may affect your plan’s compliance status but they can also offer amazing opportunities for tax savings.

Insider Tip:

We emphasize the importance of proactive compliance training for anyone involved with managing your retirement plan. Regular training sessions on the latest ERISA, IRS, and DOL updates significantly mitigate compliance risks. These sessions ensure that all administrators know their duties and the latest regulatory requirements. This proactive approach keeps your plan compliant and enhances its efficiency in providing for your employees' retirement needs.

Maximize Tax Benefits for 401k and Pension Plans with Ease

This article explored the tax benefits associated with 401k and pension contributions for employers. We provided insights into structuring contributions, avoiding common pitfalls, and staying compliant with IRS regulations.

To optimize tax benefits, employers can strategize contributions, stay informed about regulations, and seek expert guidance when needed. By implementing these strategies, you can ensure your financial planning aligns with your business goals while maximizing tax advantages.

As you reflect on the information provided, remember that navigating tax benefits for 401k and pension contributions is a continuous process. Stay proactive, stay informed, and make the most of the opportunities available to you.